For US private equity investors focused on tech and software, the search for alpha increasingly feels like a zero-sum game. With over 5,950 firms competing domestically, credit spreads normalizing, and distribution-to-NAV ratios hovering below historic averages, where should growth-oriented investors look next?

The answer may lie across the Atlantic.

The Mid-Market Mispricing

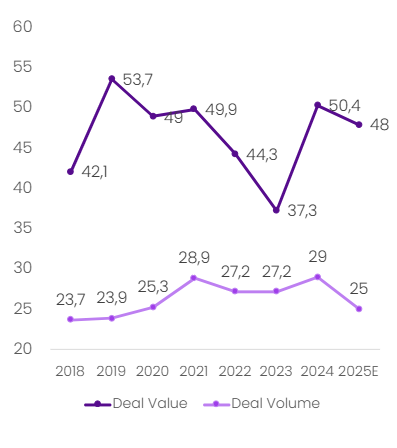

While US sponsors participated in one in four European PE deals in 2025, their activity reveals an intriguing opportunity. American capital accounted for 50% of total European deal value but only 25% of deal volume—a concentration skewed by activity toward megadeals (€1 billion+).

US PE share of UK/EU deal activity (%)

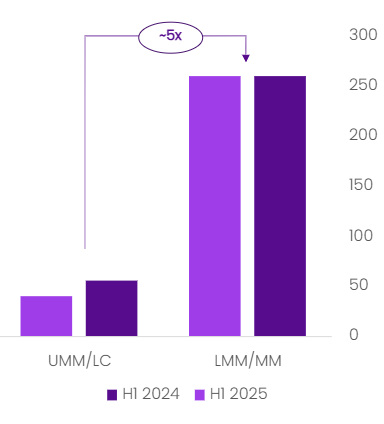

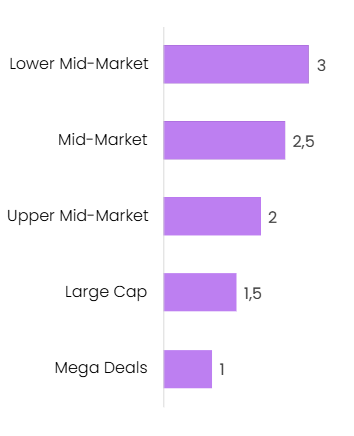

This leaves a structural arbitrage; Europe’s lower mid-market ($25-100M enterprise value) and core mid-market ($100-500M) segments contain roughly 5x transaction opportunities than large-cap deals, yet attract disproportionately less US attention. More compelling still: these segments trade at 2.5-3x multiple discounts to comparable US assets, with the lower mid-market showing the steepest gap.

European deal activity by size (#)

UK/EU valuation discount vs US (EBITDA multiple)

But here’s the provocation: if UK and EU mid-market software assets are mispriced, why haven’t European sponsors already captured this alpha? What systemic advantages do US investors possess that are limited to European counterparts—and are those advantages transferable at scale?

Escaping the Cyclicality Trap

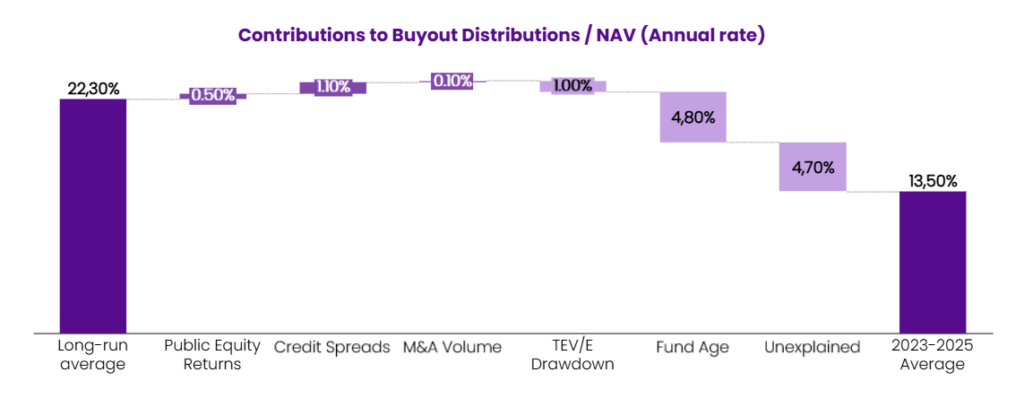

Recent research from the Institute of Private Capital reveals an uncomfortable truth: cyclical factors explain approximately 50% of the current slowdown in US PE distributions. Fund age, public market returns, credit spreads, TEV/EBITDA compression, and M&A volume collectively predict half the variance in distribution activity—variables largely outside GP control.

Contributions to Buyout Distributions / NAV (2023-2025, annual rate)

The 2025 Pitchbook European PE Breakdown confirms what sophisticated LPs already suspect: geographic diversification matters more in a post-2022 interest rate regime, which has seen DACH exits at record levels and the Nordics proved relatively insulated from trade tariff volatility.

Yet diversification alone isn’t the full story. Consider this: if European markets genuinely offer non-correlated returns, why did sponsor-to-sponsor exits account for 54% of European exit value in 2025—a market structure that theoretically should amplify, not dampen, with cyclicality? The answer reveals which investors possess the operational toolkit to extract value independent of macro conditions.

The AI Investment Arbitrage

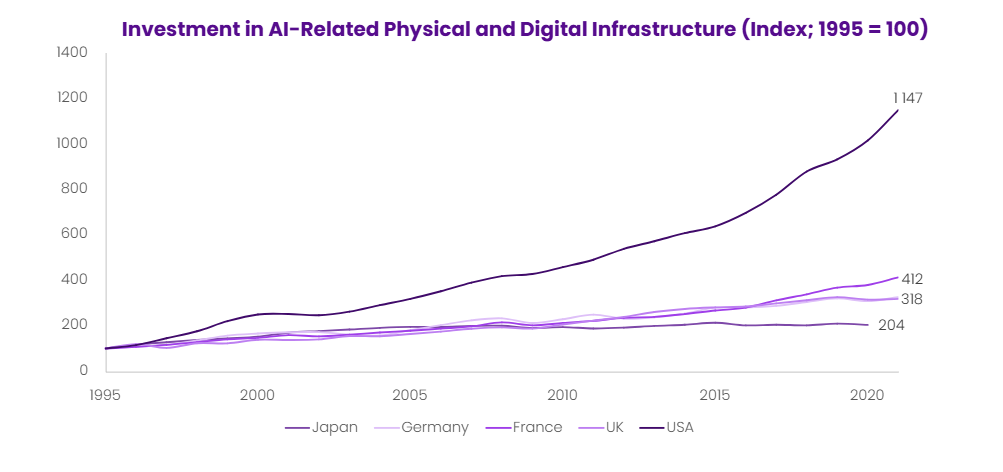

US PE’s impact on portfolio company technology adoption is well-documented: a 23% increase in IT budgets post-investment, 6% growth in digital job postings, and accelerated capital allocation to high-AI-potential firms following breakthrough events. Private equity has become the operating system for technology acceleration – and the US has been outpacing since 1995

Investment in AI-Related Physical and Digital Infrastructure (Index; 1995 = 100)

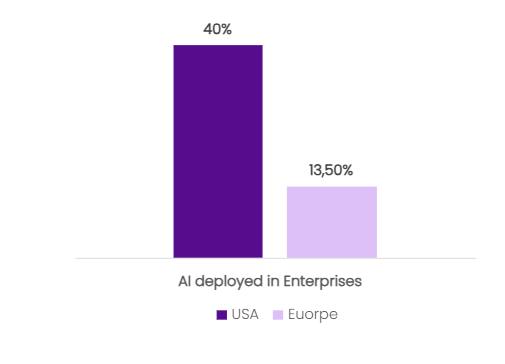

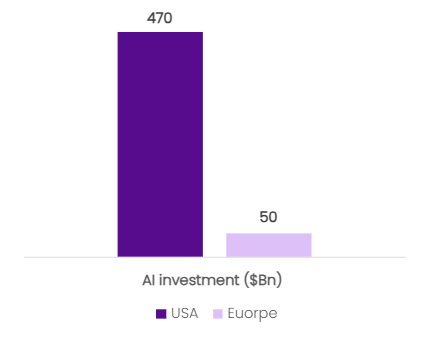

Meanwhile, Europe lags conspicuously. As of 2024, only 13.5% of EU enterprises deployed AI technologies compared to 40% US employee adoption rates. Cumulative US private AI investment through 2024 exceeded $470 billion versus roughly $50 billion in Europe—a 9:1 spending ratio. Enterprise AI budgets in the US are projected to rise 75% year-over-year, moving decisively beyond pilot spend into scaled deployment.

AI technologies deployed in enterprises (Adoption)

AI Investment up to 2025 ($ Billions)

This creates an uncomfortable question for US investors focused on domestic opportunities only: are you competing to deploy AI among companies that already possess AI maturity, or capturing returns by bringing AI maturity to companies that lack it?

The corridor strategy—building platforms in UK&I and the Nordics, scaling through DACH and Benelux, deploying selectively in CEE—has proven effective precisely because it pairs US commercial excellence with European inefficiency. LegalTech, HealthTech, vertical-ERPs, and Office of the CFO software represent high-impact, low-complexity segments where US GTM acceleration and AI-enabled operational improvement compound fastest.

The Question No One’s Asking

If European mid-market tech and software assets trade at discounts, offer portfolio diversification from US cyclicality, and present a 3-5 year window to capture the AI investment gap before Europe reaches parity—why does Europe still account for less than 30% of US PE deal volume?

Perhaps the better question is: how long will this arbitrage remain available?

Sources: Pitchbook, Silverpeak, RealDeals Media, PMP Strategy, The Federal Reserve, EUKLEMS

Author: Ben Bugg, Associate Partner, PMP Strategy UK

About PMP Strategy

PMP Strategy is an independent strategic management consulting firm distinguished by top management who bring C-level operational experience and combine deep sector expertise with strategic rigor to deliver tangible, lasting impact.

For over two decades, we have served as trusted advisors to executive committees and investors across North America, Europe, the Middle East, and Africa. We focus on sectors where complexity and disruption create opportunity : Telecoms, Media & Technology (TMT), Digital Infrastructure, Software, Private Equity, Financial Institutions, Transport & Mobility, and Industry & Energy.

Our Transversal Performance practice leads complex transformation programs across functions and geographies. Our Innovation Lab—dedicated to AI strategy, risk, and value creation—supports clients globally.

Our approach is built on partnership—designing tailored strategies alongside clients and working hand in hand to drive implementation, delivering measurable results that evolve with their ambitions.

Learn more at www.pmpstrategy.com

Press Contact:

Jennifer Campbell

+33 6 32 05 14 27

jcampbell@pmpstrategy.com