Article by PMP Strategy and Frontier Economics

Now that the EU has set its targets for SAF integration, funding must be found to finance supply if Europe is to reap the industrial benefits that SAF can offer

The “ReFuelEU Aviation” regulation (2023/2405/EU) sets an ambitious trajectory for integrating sustainable aviation fuels (SAF). However, the actual ramp-up will depend on overcoming a number of constraints: availability of inputs for SAF production, the cost differential of SAFcompared to Jet A1 (the current fossil fuel in the aviation sector) as well as industrial capacity. Ultimately, if the political target is the development of a robust and scaled-up European SAF supply chain, the key issue will be mobilising sufficient private capital despite of the callenges lined out above.

The ReFuelEU Aviation Regulation, which came into force on 1 March, sets a binding trajectory for integrating SAF into the fuel supply available at EU airports: 2% in 2025, 6% in 2030, 70% in 2050, and reflecting a gradual increase in the share of eSAF (synthetic fuel produced from sustainable electricity). These targets have one advantage: they create demand. However, they do not guarantee the development of the necessary production capacities on European soil, nor the transition to scale at the expected rate.

At a time when the Sustainable Transport Investment Plan (STIP), announced by the European Commission a few months ago, provides for a budget of €2.9 billion for sustainable fuels for aviation and maritime transport, the acceleration of SAF production in Europe will probably no longer depend on increased public budgetary support. The main challenge will now be to unlock private investment , as this will determine the speed and scale of the transition. The objective is clear: Making the sector financeable.

1) The technical dimension is no longer a limiting factor, even if the different SAF pathways need to continue maturing

The public debate still frequently sees SAF integration as a technological issue. However, the sector has reached a turning point in several areas.

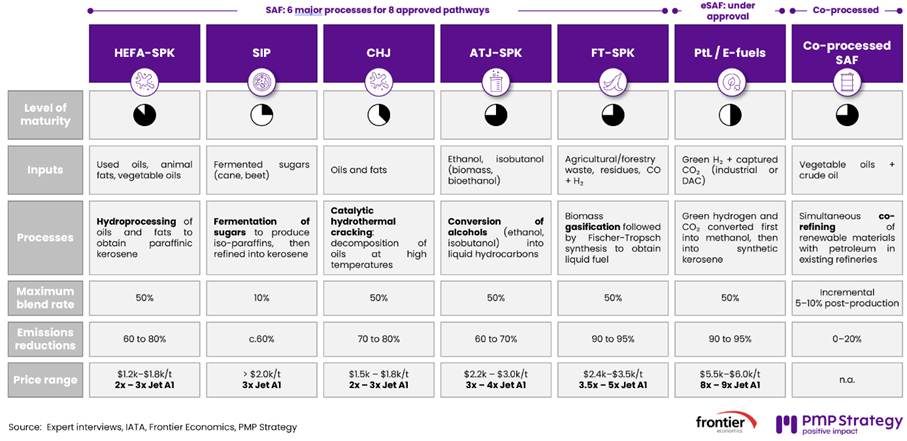

On the production side, the manufacturing processes for “neat SAF” (sustainable fuel before blending) are now well established. There are eight officially certified processes, based on several different methods and inputs and offering varying levels of environmental performance . Certain configurations enable very high lifecycle emission reductions . This is particularly the case for synthetic fuels (eSAF), provided that low-carbon electricity and appropriate (biogenic) CO₂ sources are available.

On the demand side, SAF benefit from their “drop-in” nature: they are designed to replicate the characteristics of Jet A1. Currently certified SAFs are authorised for blending with fossil kerosene at up to 50%. The remaining challenges for higher blending rates mainly concern the complete validation, over time, of certain parameters (e.g. issue of aromatics and material/seal compatibility on certain fleets), rather than structural incompatibility.

On an operational level, airport platforms have demonstrated the feasibility of integrating SAF in regular supply. Oslo airport began integrating SAF in 2016, and hubs such as LAX in Los Angeles and San Francisco airport show that SAF can be injected and distributed without major investment in existing infrastructure.

However, it would be unwise to conclude that “everything is sorted”. The sector remains constrained by major economic challenges that significantly limit the financing of European production capacity, in particular.

2) Demand for SAF is created by ReFuelEU mandates, but is hampered by its production cost, and therefore its price

Depending on the pathway and geographical location, neat SAF currently sells for between 2x and 10x the price of kerosene (excluding carbon certificates), or approximately £800 to £4,000/tonne.

- The HEFA-SPK (Hydroprocessed Esters & Fatty Acid) pathway, the most mature technology based on used oils in particular, is at the lower end of the range: x2 to x5 depending on the place of production and national subsidies;

- The ATJ-SPK (Alcohol-to-jet) process, another currently maturing technology that relies on the production of alcohol from biomass, is typically around x3 to x4;

- E-fuels, synthetic fuels that are potentially carbon-neutral if produced from sustainable energy sources and biogenic CO2, are currently priced at around x10 compared to traditional kerosene.

In the medium term, after maturation and ramp-up, a plateau of around x2 to x3 compared to fossil comparators is often mentioned for part of the volumes, which remains a significant cost differential. This differential is all the more noticeable given that with strong competition and high macroeconomic cyclicality airlines’ proftiablity is structurally constrained, with average margins typically between 6 and 9%.

Fuel currently accounts for around 30% of an airline’s operating expenses. The incorporation of 10% SAF at an average price of x3 the fossil comparator therefore results in the loss of at least two-thirds of the margin if the additional cost is not passed on to the end customer, and a net decline in competitiveness if the cost differential is not compensated elsewhere (e.g. due to penalties for airlines that are not respecting SAF mandates).

The question of “who pays?” can therefore not be avoided. The answer will depend on a number of factors – acceptability (ticket price), competitiveness and the mechanisms for sharing the additional cost between different stakeholders (airlines, fuel suppliers, corporate customers, carbon markets, or the public purse). It is all the more critical given that the most mature and least expensive pathways are also those with the most limited inputs (i.e. bio-SAF), which means that other pathways must be developed in parallel.

3) Inputs for the various SAF pathways: a structural and competitive constraint

The most mature technologies , in particular HEFA-SPK (Hydroprocessed Esters & Fatty Acid) and CHJ (Catalytic Hydrothermolysis), rely on inputs for which resource availability is structurally limited: used oils, fats or certain types of lipids. These resources are scarce, in competition with other markets (notably road biodiesel and certain maritime sectors) and exposed to risks of volatility and fraud regarding their origin.

Even assuming maximum mobilisation of the “collectable fatty waste” resource, market estimation currently consider that SAF produced from these fats would hardly cover more than 3 to 4% of global demand for sustainable kerosene by 2050, to 10% in a high-case scenario. Indeed, IATA anticipates global demand for SAF in 2050 to be around 500 Mt/year, while the maximum volumes of used cooking oil (UCO) that can be collected are currently estimated at around 60 Mt by Global Data, twice what is expected to be collected in 2030 according to S&P. The competition for resource use observed to date with the production of road and marine biofuels suggests that the aviation sector could potentially capture a third of overall volumes, based on conservative assumptions. With a mass yield of 75%, this would amount to producing 15 to 20 Mt of SAF per year, or between 3 and 4% of estimated demand. Similarly, the recovery of household waste by other sectors competes with other existing uses, such as heat production.

Beyond these estimates, the issue is not whether a single technology will ultimately be able to cover 5, 6 or 10% of the expected needs for 2050, but that the industry has no choice: it is imperative to industrialise existing mature technologies in order to accelerate production in the short and medium term, while at the same time also investing in the longer term and technology pathways that are less mature (Fischer-Tropsch-SPK, Alcohol-to-Jet-SPK, Power-to-Liquid/e-fuel), otherwise the sector would quickly reach a volume ceiling and SAF integration would stall.

4) Accelerating investment in production capacity

In mid-2025, global SAF production capacity was around 5.6 Mt/year, or 1-2% of global kerosene consumption. In Europe, capacity was around 1.4 Mt/year, or around 2.5% of European consumption, largely based on the most mature technologies (i.e. those that face strongest input limitations).

At the same time, the European regulatory trajectory is ambitious: 2% in 2025, 6% in 2030, 70% in 2050. The gap between local capacity and the regulatory trajectory highlights the need to finance and build new units in Europe, otherwise there will be a long-term dependence on imports.

However, SAF projects are long-term and capital-intensive. It often takes more than six years to build a production unit. Depending on the pathway, a facility with a capacity of 100kt/year, i.e. a medium-sized industrial site today, requires CAPEX of between $150 million (HEFA-SPK) and more than $1 billion (PtF/e-fuel). The complexity can be further amplified by the lack of maturity of upstream value chains (renewable green hydrogen production, carbon capture, etc.).

Under these conditions, the funding to be mobilised far exceeds the scale of one-off subsidies and even the investment capacities of public authorities alone. The industry needs private capital. As an order of magnitude, more than €20 billion would be needed to finance the missing capacity to meet the 2030 mandate, if SAF supply was to avoid relying on imports. Depending on the EU’s ambitions in terms of domestic production, the financing requirement would further increase significantly after 2030 as integration quotas are strengthened.

Conclusion

Europe has set an ambitious SAF trajectory that is consistent with its climate objectives. But success now depends less on a promise of demand than on the ability to develop an industrial supply chain that is financed and ready on time. Production inputs, liquid price signals and capacity constraints are not minor details: they are the determining factors of the actual ramp-up of the sector in the next years.

The main hurdle to overcome is therefore financial: making projects financeable, lowering the cost of capital, securing the development of production capacity, and efficiently sharing additional costs in a way that is compatible with the economics of air transport. The logical next step is to specify how, in concrete terms, to make this sector “bankable” and what conditions of stability can unlock large-scale private investment.

Authors :

Sébastien Charbonnel, Associate Partner at PMP Strategy

Sébastien Charbonnel is an Associate Partner at PMP Strategy, within the Transport & Energy team. Sébastien advises clients in the aviation and airport sectors, as well as investment, infrastructure and private equity funds active in the transport and energy sectors. He regularly works on issues relating to growth strategy, investment strategy, operational improvement, reorganisations, and strategic and commercial due diligence.

Lionel Chapelet, Partner at PMP Strategy

Lionel Chapelet is a Partner at PMP Strategy, within the Transport & Energy team. Lionel advises clients in the rail and airport sectors, as well as investment, infrastructure and private equity funds active in the transport sector. He regularly works on issues relating to growth strategy, investment strategy, reorganisation of business and operating models, and strategic and commercial due diligence.

Catherine Galano, Executive Director at Frontier Economics

Catherine Galano is an Executive Director at Frontier Economics and leads the firm’s activities in France. She advises French and European clients on matters of strategy, regulation and public policy, with a particular focus on the energy and transport sectors. Catherine Galano works on a range of issues including market design, infrastructure access pricing, competition, asset acquisition and sale, and public policy evaluations.

Stefan Rohm, Senior Principal at Frontier Economics

Stefan Rohm is a Senior Principal at Frontier Economics. He advises operators, investors and public authorities on all economic aspects related to essential infrastructure sectors, including economic regulation, infrastructure financing and commercial strategy. In this context, Stefan Rohm supports his clients on the future challenges facing infrastructure, including the energy transition, strategic autonomy and resilience.

About PMP Strategy

PMP Strategy is an independent International strategic management consulting firm distinguished by Partners who bring C-level operational experience and combine deep sector expertise with strategic rigor to deliver tangible, lasting impact.

For over twenty years, we have served as trusted advisors to executive committees and investors across North America, Europe, the Middle East, and Africa. We specialize in five key sectors where transformation is most critical: Telecoms, Media & Technology (TMT), Private Equity, Financial Institutions, Transport & Mobility, and Industry & Energy. Our Transversal Performance practice leads complex, cross-sector transformation programs, while our Innovation Lab—a dedicated team of AI experts—supports client engagements worldwide from our headquarters in Paris and our network of international offices.

Our approach is built on partnership—designing tailored strategies alongside clients and working hand in hand to drive implementation, delivering measurable results that evolve with their ambitions. Learn more at www.pmpstrategy.com

Press Contact:

Jennifer Campbell

+33 6 32 05 14 27

jcampbell@pmpstrategy.com